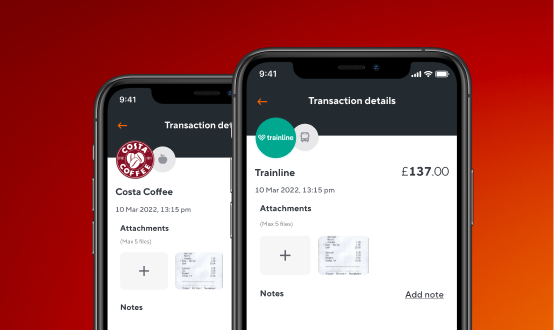

One platform for every business expense

Manage out of pocket expenses alongside your Soldo card transactions, all in one place.

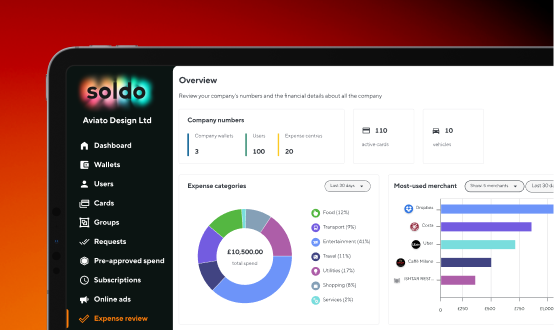

Keep control over who spends what, where

Set up spending policy profiles that match your company spending rules to simplify approvals and get complete oversight.

Cut hours of expense admin

Automate your expense reports, which also highlight reimbursements, and save time at month-end with easy expense reviews.